Code

(analytic weights assumed)

(analytic weights assumed)

(analytic weights assumed)When we care about everyone

As we saw last class, conditional quantile regressions have only one purpose:

This is a very useful tool!. As it allows you to move beyond Average relationships.

There is a limitation, however. The effects you may estimate, will depend strongly on model specification.

What if, you are interested in distributional effects across the whole population! Not only a subsample?

Common mistake when analyzing QRegressions: Make interpretations as if the average effects on the \(qth\) conditional quantiles would be the same as the effect on the “overall” \(qth\) quantile.

Except for few cases (when Quantile regressions are not relevant), CQ effects do not translate directly into Changes into the unconditional quantile.

However, as a policy maker, this would be the most relevant estimand you may be interested in :

How does improving education affect inequality?

Would eliminating Unionization would increase wage inequality?

Is there heterogeneity in consumption expenditure?

However, going from Conditional to unconditional statistics (not only Q) is not always straight forward.

One of the questions I read a lot regarding UQR is what do we mean unconditional?

This is perhaps a someone poor choice of words.

Anytime we estimate ANY statistic, we condition on something.

We condition on all individual characteristics (including errors)

We condition on groups characteristics (CQREG and CEF)

or, We condition on all characteristics (distributions). We happen to call this, unconditional statistics.

This, however, does make a big difference in interpretation.

\[\begin{aligned} y_i &= b_0 + b_1 x_i + e_i + x_i e_i \\ \frac{dy_i}{dx_i}&=b_1 + e_i \\ E(y_i|x_i=x) &= b_0 + b_1 x \\ \frac{dE(y_i|x)}{dx}&=b_1 \\ E(E(y_i|x_i=x))=E(y_i) &= b_0 + b_1 E(x_i) \\ \frac{dE(y_i)}{dE(x_i)}&=b_1 \end{aligned} \]

Same effects, but different interpretations (specially last one)

Consider any distributional statistic \(v\), which takes as arguments, all observations, density distributions \(f()\), or cumulative distributions \(F()\).

\[ v = v(F_y) \ or \ v(f_y) \ or \ v(y_1, y_2, ...,y_n) \]

And to simplify notation, lets say this function is defined as follows:

\[ v(f_y) = \int_{-\infty}^\infty h(y,\theta) f(y)dy \]

This simply considers distributional statistics \(v\) that can be estimated by simply integrating a transformation of \(h(y,\theta)\) given a set of parameters \(\theta\).

But for now, lets consider only the Identify function \(h(y,\theta)=y\)

but…What about Controls??

Assume there is a joint distribution of function \(f(y,x)\), then

\[ \begin{aligned} f(y,x)&=f(y|x)f(x) \\ f(y) &= \int f(y|x) f(x) dx \end{aligned} \]

And all together:

\[ \begin{aligned} v(f_y) &= \int y \int f(y|x) f(x) dx \ dy \\ v(f_y) &= \iint y f(y|x) dy \ f(x) dx \\ v(f_y) &= \int E(y|X) f(x) dx \\ \end{aligned} \]

\[ v(f_y) = \iint h(y,\theta) f(y|x)f(x)dxdy \]

So, the statistic \(v\) will change if:

- We change the function \(h\) or its parameters \(\theta\).

- Assume some shocks that change the conditional \(f(y|x)\)

- or the distribution of characteristics change!

Note: \[f(y|x) \sim \beta \text{ and } f(x) \sim x \]

In an ideal scenario, you simple get the data under two regimes (before and after changes in \(x\)), and do the following:

\[\Delta v = v(f'_y)-v(f_y) \]

That is, just estimate the statistic in two scenarios (\(f'\) and \(f\)), and calculate the difference. (impossible!)

But there are (at least) three alternatives:

Consider the following

There is a policy such that you plan to improve education in a country.

Every single person will have at least 7 years of education, and will have free access to two additional years of education if they want to.

In other words, characteristics change from \(f(x) \rightarrow g(x)\) . But you do not see this!

\[ v(g_y) = \iint h(y,\theta) f(y|x) \color{red}{g(x)}dxdy \]

but perhaps, we could see this:

\[\hat v(g_y) = \iint h(y,\theta) f(y|x) \color{red}{\hat w(x)}f(x) dxdy \]

if we can come up with a set of weights \(\color{red}{\hat w(x)}\) such that \(f(x)\hat w(x)=g(x)\)

\[ \hat w(x) = \frac{\hat g(x)}{\hat f(x)} \]

Simple, yet hard. Estimation of multivariate densities can be a difficult task.

\[ f(x) = h(x|s=0) ; g(x) = h(x|s=1) \]

This makes things “easier”.

\[ \begin{aligned} h(x|s=k) &= \frac{h(x)p(s=k|x)}{p(s=k)} \\ \hat w(x) &= \frac{h(x)p(s=1|x)}{h(x)p(s=0|x)}\frac{p(s=0)}{p(s=1)} \\ &=\frac{p(s|x)}{1-p(s|x)} \frac{1-p(s)}{p(s)} \end{aligned} \]

Easier to estimate conditional probabilities, (logit probit or other) than Densities

Goal: Evaluate the impact of an increase in Fines on # of citations. (using reweighting)

webuse dui, clear

** Create Fake Sample

gen id = _n

expand 2

bysort id:gen smp = _n ==2

** Now you have two of ever person. So lets do some Policy

** Fines increase lower fines more than higher ones, up to 12

** Here we have a simulation of a policy that increases fines

replace fines = 0.1*(12-fines)+fines if smp==1(Fictional data on monthly drunk driving citations)

(500 observations created)

(498 real changes made)Estimation of Logit (or Probit) to estimate \(p(s|x)\)

And estimate IPW weights

** Estimate logit

qui:logit smp c.fines##c.fines taxes i.csize college

predict pr_smp

gen wgt = pr_smp / (1-pr_smp)

replace wgt = 1 if smp==1(option pr assumed; Pr(smp))

(500 real changes made)Have the IPW weights helped simulate the policy?

i.csize _Icsize_1-3 (naturally coded; _Icsize_1 omitted)

(analytic weights assumed)

Summary statistics: Mean

Group variable: smp

smp | fines _Icsiz~2 _Icsiz~3 college taxes

---------+--------------------------------------------------

0 | 10.10573 .2919004 .3571831 .2483835 .7047717

1 | 10.10568 .29 .358 .248 .704

---------+--------------------------------------------------

Total | 10.10571 .2909501 .3575916 .2481917 .7043858

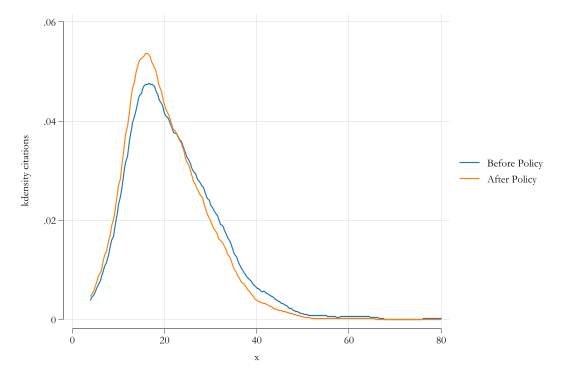

------------------------------------------------------------I can now compare the distribution of fines before and after the policy

(analytic weights assumed)

(analytic weights assumed)

(analytic weights assumed)Seems to be a contraction of # citations:

Before Policy

Variable | p10 p25 p50 Mean p75 p90

-------------+------------------------------------------------------------

citations | 11.5 15 20 22.018 27 34.5

--------------------------------------------------------------------------

After Policy

(analytic weights assumed)

Variable | p10 p25 p50 Mean p75 p90

-------------+------------------------------------------------------------

citations | 11 14 19 20.29751 25 32

--------------------------------------------------------------------------What about Standard errors? Bootstrap! (logit and estimation, probably clustering at individual level)

Easy to extend to other Statistics, but, can only provide results “within” support.

Say that you are interested in the same Policy, but do not trust re-weighting. Instead you want to model the Outcome, using some parametric or nonparametric analysis

Options for flexible mode?

You can use Heteroskedastic OLS \(y\sim N(x\beta,x\gamma)\) and predict from here

You can use CQregressions to simulate the results.

One of this is similar to what we do in simulation analysis, and imputation. The other is similar to the work of Machado Mata (2005) and Melly(2005). Where you invert the whole distribution “globally”

Model \(Y=G(X,\theta)\)

Create a “policy” \(X'=H(X)\)

Predict \(Y'=G(X',\theta)\) and identify effect:

\[\Delta V(Y) = V(Y')-V(Y)\]

Repeat many times, and summarize results.

** Example for OPT2

webuse dui, clear

** Modeling OLS with heteroskedastic errors

hetregress citations fines i.csize college taxes , het(fines i.csize college taxes )

------------------------------------------------------------------------------

citations | Coefficient Std. err. z P>|z| [95% conf. interval]

-------------+----------------------------------------------------------------

citations |

fines | -6.18443 .3018298 -20.49 0.000 -6.776006 -5.592855

|

csize |

Medium | 4.683941 .5028377 9.32 0.000 3.698397 5.669484

Large | 9.655742 .5261904 18.35 0.000 8.624428 10.68706

|

college | 4.495635 .5283579 8.51 0.000 3.460072 5.531197

taxes | -3.640864 .4938209 -7.37 0.000 -4.608735 -2.672993

_cons | 79.48011 3.118008 25.49 0.000 73.36892 85.59129

-------------+----------------------------------------------------------------

lnsigma2 |

fines | -.5261208 .082495 -6.38 0.000 -.687808 -.3644337

|

csize |

Medium | .331204 .1681709 1.97 0.049 .0015952 .6608129

Large | .5578834 .1662309 3.36 0.001 .2320768 .8836899

|

college | .3186815 .1539424 2.07 0.038 .0169599 .6204032

taxes | -.3988692 .1437708 -2.77 0.006 -.6806548 -.1170836

_cons | 8.257714 .8201063 10.07 0.000 6.650335 9.865093

------------------------------------------------------------------------------

LR test of lnsigma2=0: chi2(5) = 75.42 Prob > chi2 = 0.0000

** make Policy

clonevar fines_copy = fines

replace fines = 0.1*(12-fines)+fines

predict xb, xb

predict xbs, sigma

** Simulate results

capture program drop sim1

program sim1, eclass

capture drop cit_hat

gen cit_hat = rnormal(xb,xbs)

qui:sum citations, d

local lp10 = r(p10)

local lp25 = r(p25)

local lp50 = r(p50)

local lpmn = r(mean)

local lp75 = r(p75)

local lp90 = r(p90)

qui:sum cit_hat, d

matrix b = r(p10)-`lp10',r(p25)-`lp25', r(p50)-`lp50' , r(mean) -`lpmn',r(p75)-`lp75',r(p90)-`lp90'

matrix colname b = p10 p25 p50 mean p75 p90

ereturn post b

end

simulate, reps(1000): sim1

sum

-------------+---------------------------------------------------------

_b_p10 | 1,000 -1.08147 .3913698 -2.31713 .1689796

_b_p25 | 1,000 -.3262908 .3230118 -1.817808 .6465259

_b_p50 | 1,000 -.2085465 .316455 -1.09237 .7785921

_b_mean | 1,000 -1.675626 .2234377 -2.400322 -1.03909

_b_p75 | 1,000 -1.541725 .4210822 -2.857586 -.2505198

-------------+---------------------------------------------------------

_b_p90 | 1,000 -3.543298 .6079578 -5.464802 -1.682991Effects larger than Reweigthing. Statistical inference here may be flawed. (first stage error not carried over)

webuse dui, clear

gen id = _n

** Expand to 99 quantiles

expand 99

bysor id:gen q=_n

** make policy

gen fines_policy=0.1*(12-fines)+fines

gen fines_copy =fines

** Estimate 99 quantiles (in theory one should do more..but choose at random)

ssc install qrprocess // Faster than qreg

** Save Cit hat (prediction)

** cit policy (with policy)

gen cit_hat=.

gen cit_pol=.

forvalues i = 1 / 99 {

if `i'==1 _dots 0 0

_dots `i' 0

qui {

local i100=`i'/100

capture drop aux

qrprocess citations c.fines##c.fines (i.csize college taxes) if q==1, q(`i100')

** predicts the values as if they were in q100

predict aux

replace cit_hat=aux if q==`i'

drop aux

replace fines = fines_policy

predict aux

replace cit_pol=aux if q==`i'

replace fines = fines_copy

}

}

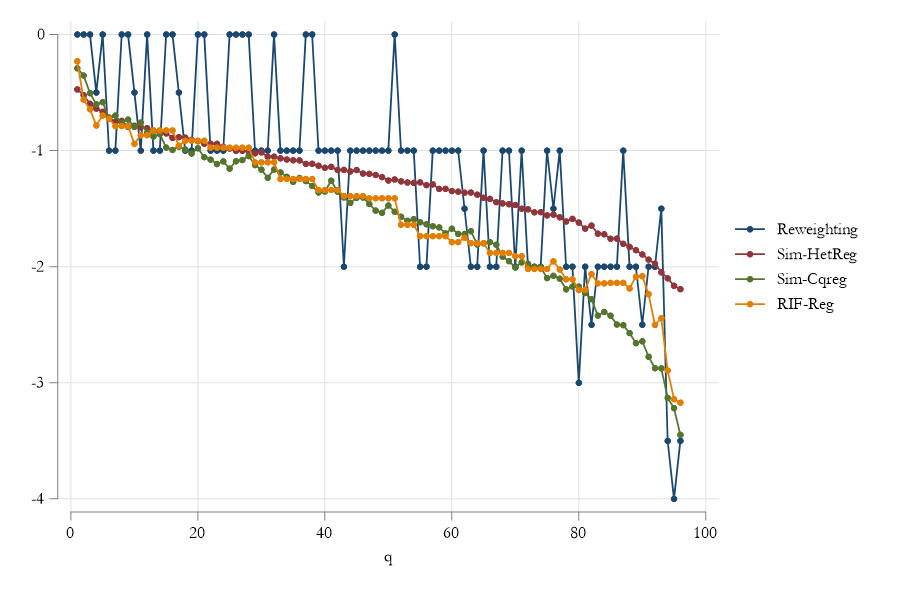

tabstat citations cit_hat cit_pol, stats(p10 p25 p50 mean p75 p90)

Stats | citati~s cit_hat cit_pol

---------+------------------------------

p10 | 11.5 10.70744 9.911633

p25 | 15 15.42857 14.27302

p50 | 20 21.15557 19.68303

Mean | 22.018 22.0002 20.31824

p75 | 27 27.65936 25.56173

p90 | 34.5 34.03413 31.39192

----------------------------------------Very demanding (computationally) and may only capture effects to the extend that we have good coverage of the distribution.

Standard Errors…Bootstrapping. Perhaps use random quantile assignment, and may have problems near boundaries.

The first option allow you to estimate effects of changes in \(f(x)\) on the unconditional distribution of \(y\), and in consequence, the distributional statistics of interest.

The second option allows you to estiamte those effects by modeling the conditional distribution of \(y\) or \(E(y|x)\).

They have limitations:

The third approach was first introduced by Firpo, Fortin and Lemieux 2009, as a computationally simple way to analyze how changes in \(X's\) affect the unconditional quantiles of \(y\).

This strategy was later extended to analyze the effects on a myriad of distributional statistics and rank dependent indices, as well as an approach to estimate distributional treatment effects.

See Rios-Avila (2020).

In contrast with other approaches, it can be used to analyze multiple types of policies without re-estimating the model. However the identification and interpretation needs particular attention.

It also allows you to easily make Statistical inference. (except for quantiles…)

Reconsider the Original question. How do you capture the effect of changes of distribution of \(x\) on the distribution of \(y\).

\[ \Delta v=v(G_y) - v(F_y) \]

Now, assume that \(G_y\) is just marginally different from \(F_y\) (different in a very particular way)

\[ G_y(y_i) = (1-\epsilon)F_y+ \epsilon 1(y>y_i) \]

This function puts just a bit more weight on observation \(y_i\). Think of it as “dropping” a new person in the pool.

If this is the case, the \(\Delta v(y_i)\) Captures how would the Statistic \(v\) changes if the distribution puts just a bit extra weight on 1 observation. (this would be very small)

Lets Rescale it:

\[ IF(v,F_y,y_i) =lim_{\epsilon \rightarrow 0} \frac{v(G_y(y_i))-v(F_y)}{\epsilon} \]

The influence function is a measure of direction of change, we should expect the statistic \(v\) will have as we change \(F_y \rightarrow G_y\) .

From here the RIF is just \(RIF(v,F_y,y_i) = v + IF(v,F_y,y_i)\)

Which has some properties:

\[ \begin{aligned} \int IF(v,F_y,y_i)f_ydy=0 &; \int RIF(v,F_y,y_i)f_y dy=v \\ v(F_y) \sim N \left(v(F_y),\frac{\sigma^2_{IF}}{N} \right) &; \int IF^2f_ydy =\sigma^2_{IF} \end{aligned} \]

First:

\[ v(F_y) = \iint RIF(v,F_Y,y_i) f(y|x)f(x)dy = \int E(RIF(.)|x) f(x) \]

From here is similar to Opt 3. Use some econometric model to estimate \(E(RIF(.)|X)\), and use that to make predictions on how \(v(F_y)\) would change, when there is a distributional change in \(X\).

RIF-OLS: Unconditional effect!

\[ RIF(v,F_y,y_i) = X\beta+e \ \rightarrow\ E(RIF) = v(F_y) = \bar X \beta \\ \frac{dv(F_y)}{d\bar X}=\beta \]

Logic. When \(F_x\) changes, it will change the distribution of \(F_y\), which will affect how the statistic \(v\) will change. But, we can only consider changes in means! (and Var)

RIF regressions works by using a linear approximation of the statistic \(v\) with the changes in \(F_y\) which are caused by changes in \(F_x\), proxied by changes in \(\bar X\).

Depending on the model specification, however, we may only be able to identify changes in first and second moments of the distribution of \(x\). (Mean and variance).

-

However, as any linear approximation to a non-linear function, the approximations are BAD when the changes in \(F_x\) are too large. The most relevant example…Dummies and treatment!

Dummies are a challenge. At individual or conditional level, we usually consider changes from 0 to 1 (off or on).

For unconditional effects this is not correct (too large of a change) (No-one treated vs All treated). Thus you need to change the question…Not on and off changes, but Changes in proportion of treated!

However, its possible to restructure RIF regressions to be partially conditional (Rios-Avila and Maroto 2023) (Combines CQREG with UQREG)

Similar problems are experienced if the change in continuous variables is large!

webuse dui, clear

** Consider the policy change

gen change_fines= 0.1*(12-fines)

** consider average change in fines.Since we are only considering this effect

sum change_fines

rifhdreg citations fines i.csize college taxes, rif(q(10))

est sto m1

rifhdreg citations fines i.csize college taxes, rif(q(50))

est sto m2

rifhdreg citations fines i.csize college taxes, rif(q(90))

est sto m3

** This are Rescaled to show true effect

rifhdreg citations fines i.csize college taxes, rif(q(10)) scale(.21048)

est sto m4

rifhdreg citations fines i.csize college taxes, rif(q(50)) scale(.21048)

est sto m5

rifhdreg citations fines i.csize collegetaxes, rif(q(90)) scale(.21048)

est sto m6

. esttab m1 m2 m3 m4 m5 m6, se mtitle(q10 q50 q90 r-q10 r-q50 r-q90) compress nogaps

----------------------------------------------------------------------------------------

(1) (2) (3) (4) (5) (6)

q10 q50 q90 r-q10 r-q50 r-q90

----------------------------------------------------------------------------------------

fines -4.476*** -6.700*** -9.887*** -0.942*** -1.410*** -2.081***

(0.491) (0.493) (0.978) (0.103) (0.104) (0.206)

1.csize 0 0 0 0 0 0

(.) (.) (.) (.) (.) (.)

2.csize 4.603*** 7.325*** 6.370*** 0.969*** 1.542*** 1.341***

(0.963) (0.966) (1.917) (0.203) (0.203) (0.404)

3.csize 6.504*** 13.54*** 12.97*** 1.369*** 2.851*** 2.729***

(0.914) (0.917) (1.820) (0.192) (0.193) (0.383)

college 2.922** 5.948*** 9.973*** 0.615** 1.252*** 2.099***

(0.890) (0.892) (1.771) (0.187) (0.188) (0.373)

taxes -3.279*** -3.303*** -8.319*** -0.690*** -0.695*** -1.751***

(0.842) (0.844) (1.676) (0.177) (0.178) (0.353)

_cons 53.71*** 81.04*** 129.2*** 11.30*** 17.06*** 27.20***

(4.964) (4.977) (9.880) (1.045) (1.048) (2.080)

----------------------------------------------------------------------------------------

N 500 500 500 500 500 500

----------------------------------------------------------------------------------------RIF Regressions are useful, but again, one must use them with care.

Except for Stata (see rif and rifhdreg), the applications of RIF regressions outside Mean, Variance and Quantiles are non-existent. (paper?)

\[ \begin{aligned} RIF(mean,y_i,F_y) &= y_i \\ RIF(variance,y_i,F_y) &= (y_i-\bar y)^2 \\ RIF(Q,y_i,F_Y) &= Q_y(\tau) + \frac{\tau-1(y_i \leq Q_y(\tau))}{f_Y(y_i)} \end{aligned} \]

Except for quantile related functions! (\(f_y\) also needs estimation, thus errors!)

\[ RIF(.,y) = b_0 + b_1 x + b_2 (x-\bar x)^2+\varepsilon \]

\[ RIF(.,F_{Y|D},y) = b_0 + b_1 D+b_2 x + b_3 (x-\bar x)^2+\varepsilon \]

Because this implementation uses LR, you can add Multiple Fixed effects as well. (with limitations)

And you can skip LR all together, and model RIF using Other approaches! (which may be even better than OLS).

Truly going nonlinear. When \(\beta\) is no longer linear in \(y\) (nor is the error)